Architecture Billings Declined Slightly in February

Multi-family billings have been negative for 43 consecutive months.

Architecture Billings Index in Contraction for 38 of Last 41 Months

This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment including multi-family residential.

From the AIA: ABI February 2026: Business conditions at architecture firms may stabilize soon

The AIA/Deltek Architecture Billings Index® (ABI) score for the month was 49.4, meaning that the share of firms reporting that billing declined was only slightly greater than the share of firms reporting that billings increased (a score of 50 would mean that those shares were equal). In addition, inquiries increased again this month, after declining slightly in January. And while the value of newly signed design contracts continued to decline, the pace of that decline slowed significantly. All these signs suggest that business conditions at architecture firms may be stabilizing, though ongoing global economic uncertainty may make that short-lived.

Business conditions remained flat at architecture firms located in the South for the second consecutive month in February but continued to decline at firms located in other parts of the country. Billings were particularly soft at firms in the Northeast, most likely due to the recent parade of winter storms that have hit the region. Firms across all specializations continued to experience declining billings this month, but the share of firms with an institutional specialization reporting declining billings decreased, as billings at those firms approached flat.

...

The ABI serves as a leading economic indicator that leads nonresidential construction activity by approximately 9-12 months.

emphasis added

• Northeast (41.9); Midwest (46.3); South (50.0); West (47.2)

• Sector index breakdown: commercial/industrial (45.7); institutional (49.2); multifamily residential (48.2)

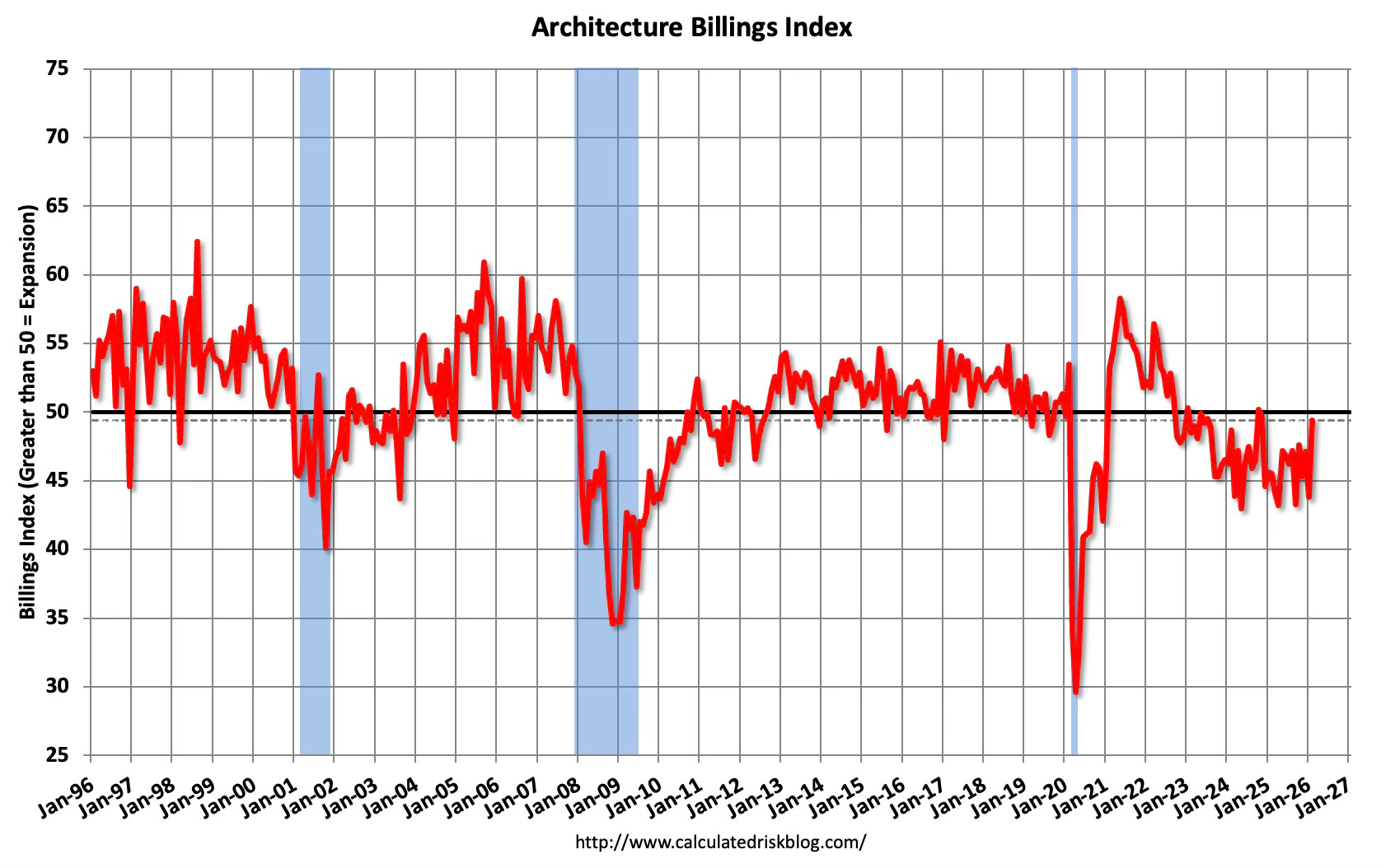

This graph shows the Architecture Billings Index since 1996. The index was at 49.4 in February, up from 43.8 in January. Anything below 50 indicates a decrease in demand for architects’ services. This index has indicated contraction for 38 of the last 41 months.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions. This index typically leads CRE investment by 9 to 12 months, so this index suggests a slowdown in CRE investment throughout 2026.

Multi-family billings have been below 50 for 43 consecutive months. This suggests we will some further weakness in multi-family starts.