Black Knight Mortgage Monitor for December

"Worst affordability levels since 2008"

Black Knight publishes a monthly Mortgage Monitor report that contains interesting information on the mortgage market and housing.

Today, the Data & Analytics division of Black Knight, Inc. (NYSE:BKI) released its latest Mortgage Monitor Report, based upon the company's industry-leading mortgage, real estate and public records datasets. After a year of historic home price gains, homeowners' tappable equity – the amount available for a mortgage-holder to access while retaining at least a 20% equity stake in their home – has hit yet another record high. According to Black Knight Data & Analytics President Ben Graboske, Q4 2021's nearly half-billion-dollar increase in tappable equity has also resulted in the lowest total market leverage on record.

"Home price appreciation over the course of 2021 was unlike anything that's come before, and the incredible growth we've seen in homeowner equity is testament to that fact," said Graboske. "The aggregate total of $9.9 trillion represents an astounding 35% annual growth rate – which works out to an increase of $2.6 trillion in tappable equity in a single year. …"The interplay between prices and rates has significantly impacted affordability and borrower buying power in recent weeks. It now takes 25.8% of the median household income to purchase the average-priced home with 20% down and a 30-year mortgage, up from the 22.4% required at the end of Q3 2021. Interest rate jumps in recent weeks have pushed us – and quite quickly – above the long-term, pre-Great Recession average payment-to-income ratio of 25%, straight to the worst affordability levels since 2008.”

emphasis added

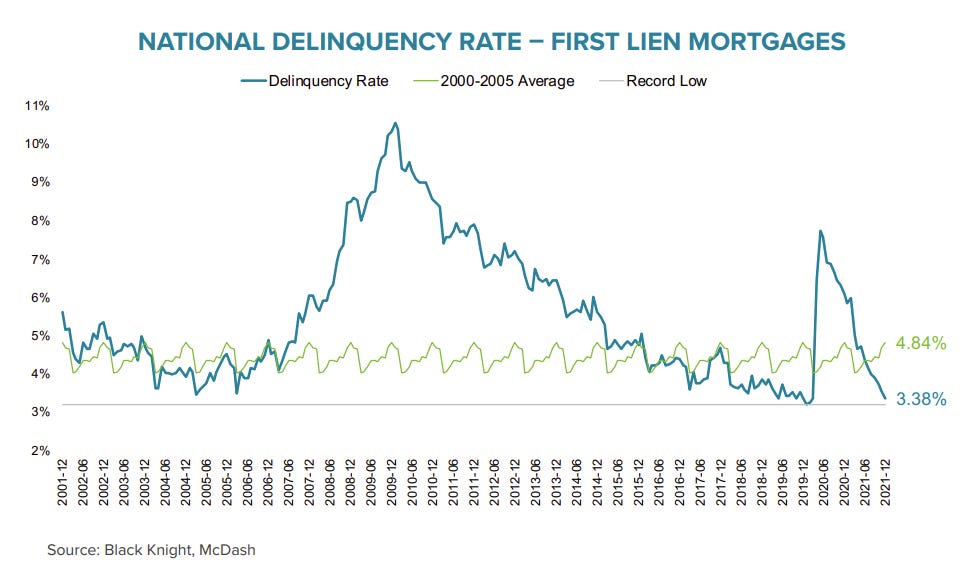

Here is a graph on delinquencies from Black Knight:

• At 3.38%, the national delinquency rate is within 0.1% of its pre-pandemic level and very near the record low set in January 2020

• There are 35% fewer early-stage delinquencies than at the start of the pandemic, but nearly 2.5 times as many serious ones – although that metric is improving as well, albeit more slowly

• The decline in serious delinquencies has been slower than might be expected given the large number of borrowers who have exited forbearance plans in recent months and remain in loss mitigation

• The share of borrowers who have exited forbearance but are unable to make full or modified mortgage payments is worth watching

• At 946K, there are still at least half a million more seriously delinquent mortgages (including those in active forbearance plans) than prior to the pandemic

And on the payment to income ratio:

• It now takes 25.8% of the median household income to purchase the average home with 20% down and a 30-year mortgage, up from the 22.4% required at the end of Q3 2021

• Interest rate jumps in recent weeks have pushed us rapidly above the long-term, pre-Great Recession average payment-to-income ratio of 25%, resulting in the worst affordability levels since 2008

• While a 20.5% ratio has been the tipping point between market acceleration and deceleration over the past decade, severe inventory shortfalls are keeping home prices running hotter than they might otherwise

There is much more in the mortgage monitor.