Case-Shiller National Index up 19.2% Year-over-year in January

calculatedrisk.substack.com

Case-Shiller National Index up 19.2% Year-over-year in January

FHFA: "House prices continued to climb but not as rapidly during the final quarter of 2021 as in earlier quarters"

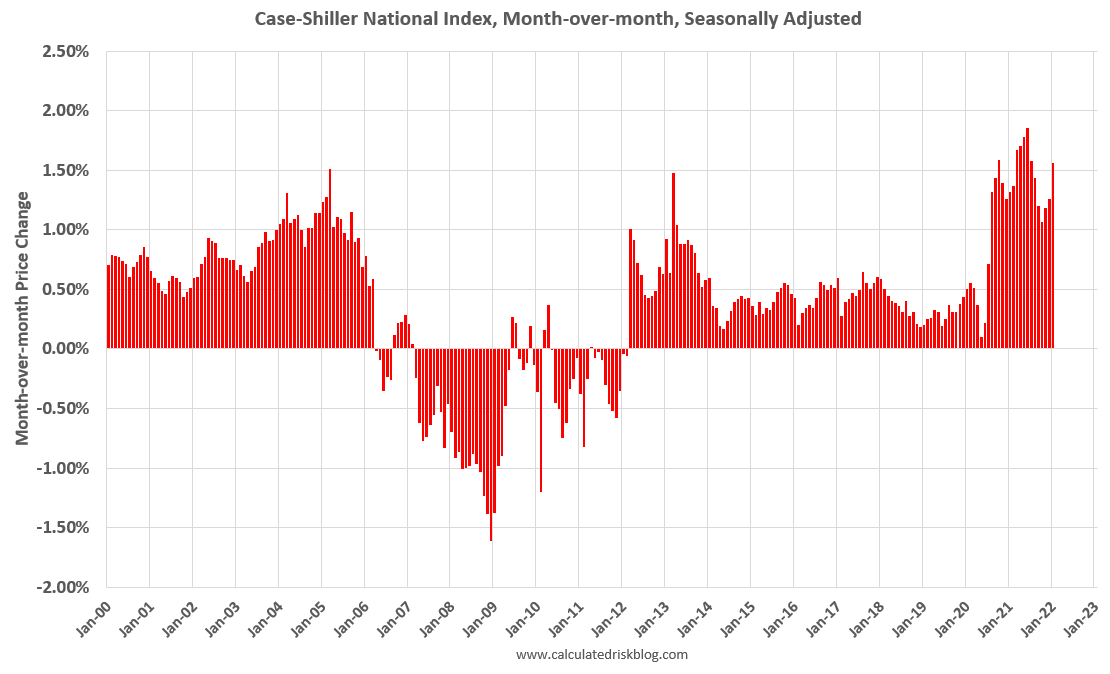

Both the Case-Shiller House Price Index (HPI) and the Federal Housing Finance Agency (FHFA) HPI for January were released today. Here is a graph of the month-over-month (MoM) change in the Case-Shiller National Index Seasonally Adjusted (SA).

The MoM increase in Case-Shiller was at 1.56%. This is the seventh strongest MoM increase in the Case-Shiller in…

Keep reading with a 7-day free trial

Subscribe to CalculatedRisk Newsletter to keep reading this post and get 7 days of free access to the full post archives.