House Prices Increase Sharply in June

Both the Case-Shiller House Price Index (HPI) and the Federal Housing Finance Agency (FHFA) HPI were released today.

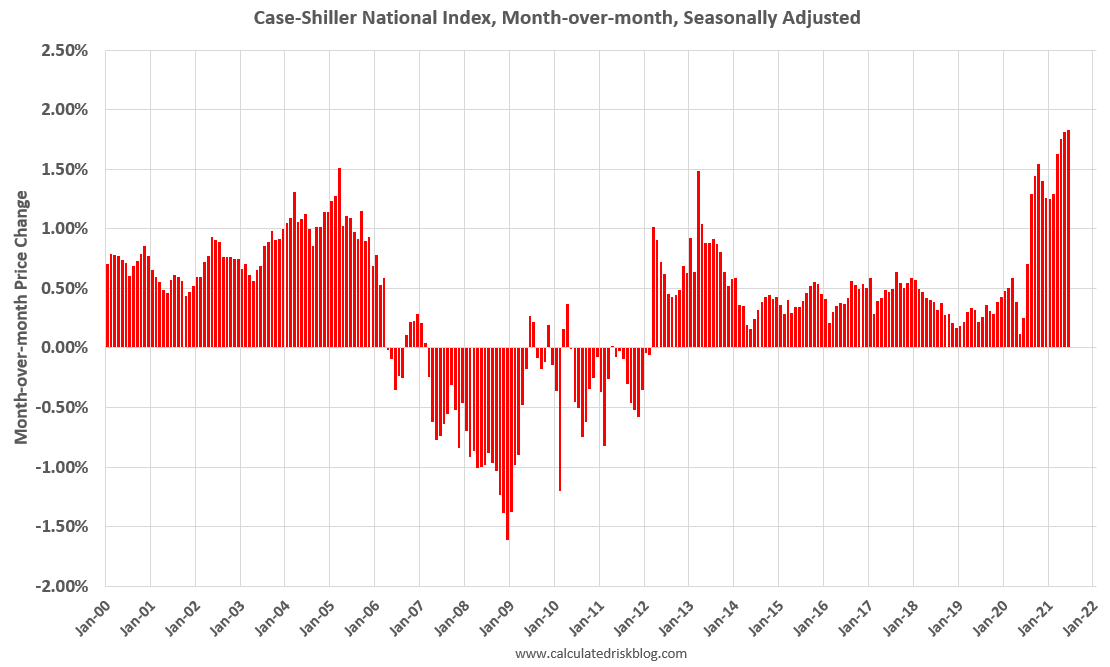

First, here is a graph of the month-over-month change in the Case-Shiller National Index (SA).

The last four months have all seen record month-over-month price increases, and the last 11 months have all been historically very strong.

FH…

Keep reading with a 7-day free trial

Subscribe to CalculatedRisk Newsletter to keep reading this post and get 7 days of free access to the full post archives.