June ICE Mortgage Monitor: Home Prices Continue to Cool

Here is the ICE June Mortgage Monitor report (pdf).

Press Release: ICE Mortgage Monitor: Record Levels of Home Equity and Falling Rates Drive Highest HELOC Withdraws Since 2008

Intercontinental Exchange, Inc. … today released its June 2025 Mortgage Monitor report. The analysis of mortgage, real estate and public records data shows U.S. mortgage holders carried a record $17.6 trillion in home equity entering the second quarter of 2025, with $11.5 trillion considered “tappable” — that is, available for borrowing while maintaining at least a 20% equity cushion.

Despite subdued withdrawal rates in recent years, early 2025 data points to shifting borrower behavior. First-quarter second lien equity withdrawals rose 22% year over year to nearly $25 billion — the largest first quarter volume in 17 years — suggesting increased interest in home equity access amid improving loan affordability.

“Equity levels remain historically high, and now we’re seeing the cost of borrowing against that equity drop meaningfully,” said Andy Walden, Head of Mortgage and Housing Market Research at ICE. “The monthly payment needed to withdraw $50,000 via a home equity line of credit (HELOC) has fallen by more than $100 since early 2024. If the Fed moves forward with anticipated rate cuts, borrowing against home equity could become even more attractive in the second half of the year.” …

Other highlights from the June 2025 Mortgage Monitor include:

48 million mortgage holders have tappable equity, with the average homeowner sitting on $212K.

Mortgaged homes are, on average, only 45% leveraged, suggesting ample cushion for equity access.

Lenders are becoming more aggressive with their HELOC rate offerings, with the spread to prime falling to the lowest levels since 2022.

Equity withdrawals — including cash-out refinances — totaled $45 billion in the first quarter of 2025, the highest first quarter volume since 2022.

Borrowers tapped just 0.41% of available tappable equity in the first quarter of 2025, still below long-term averages, indicating further room for growth.

“In our latest ICE Borrower Insights Survey, roughly 25% of homeowners said they are considering a home equity loan or HELOC in the next year. It’s periods like these — where both demand and affordability trends converge — that represent a critical opportunity for housing finance professionals to earn homeowners’ repeat business,” said Tim Bowler, President of ICE Mortgage Technology.

emphasis added

Mortgage Delinquencies “Steady” in April

Here is a graph of the national delinquency rate from ICE. Overall delinquencies decreased in March and are below the pre-pandemic levels. Source: ICE McDash

Overall, mortgage delinquencies held relatively steady in April with the national delinquency (DQ) rate rising by just 1 basis point (bp) to 3.22% in the month

A wider scope shows that while mortgage performance still remains historically strong, delinquency and foreclosure metrics are gradually trending higher on a year-over-year basis

The national DQ rate is up 13 bps (4.1%) YoY and while serious delinquencies (SDQs) ‒ loans 90+ days past due but not in foreclosure ‒ improved seasonally in April, they were up 14% YoY, continuing a six-month streak of 10%+ increases

Foreclosure starts (+13%), sales (+9%), and active inventory (+4%) all rose YoY for the second consecutive month

April’s 6,500 foreclosure sales marked the largest single-month volume in 15 months, with VA sales, which account for the bulk of the recent rise, hitting their highest level since 2019

Hurricane-related SDQs fell 5,300 to roughly 18K, from November’s peak of 58K, driving 30% of the -3.7% overall improvement

Inventory Increasing Sharply, Significant Regional Differences

This graph shows ICE’s estimate of the National inventory deficit (change from 2017 - 2019 levels).

The number of homes available for sale is up +30% from the same time last year, with shortage from pre-pandemic levels having fallen to -16%, down from -36% at this time last year, the lowest deficit since early 2020

That deficit was cut by 4 percentage points in April alone, marking one of the largest single-month gains since 2022

At the current rate of improvement, inventory would return to pre-pandemic levels nationally by mid-2026

37 of the 100 largest markets have already seen their inventory levels normalize, with Denver now surpassing TX and FL markets for the largest inventory surplus, with 90% more homes for sale compared to its 2017-2019 April average

Inventory growth has largely come from a slowing of sales volumes, although new listings have slowly begun to return as well

Through the first 4 months of 2025, new listings have run 15% below their 2017-2019 averages, and while that’s still below ‘normal’ levels, it’s an improvement from the -22% deficit we averaged early last year

This graph illustrates the significant regional differences with inventory growth. The Northeast and Upper Midwest still have low levels of inventory. Meanwhile, prices are falling in part of Florida and Texas - and other cities with inventory above 2017 - 2019 levels.

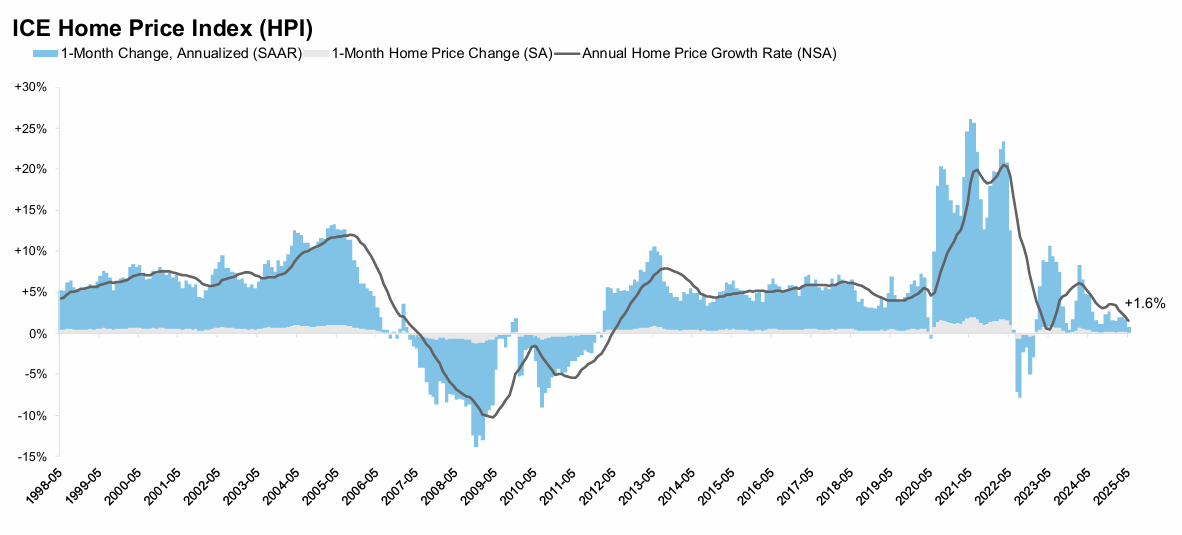

House Price Growth Continues to Slow

Here is the year-over-year in house prices according to the ICE Home Price Index (HPI). The ICE HPI is a repeat sales index. ICE reports the median price change of the repeat sales. The index was up 2.0% year-over-year in April, down from 2.4% YoY in March. The early look at the May HPI shows a 1.6% YoY increase.

Improved inventory levels are providing more options and a softer price dynamic for homeowners shopping this spring

Annual home price growth cooled to a revised +2.0% in April from +3.6% at the start of the year, with ICE’s Home Price Index suggesting price growth cooled further to +1.6% in May, the slowest growth rate in nearly two years

May data also shows home prices rose by a modest 0.1% in the month on a seasonally adjusted basis, which would mark the softest single-month growth since late 2023, when mortgage rates climbed above 7.5%

If recent seasonally adjusted gains persist, the annual home price growth rate is poised to cool further

Single family prices were up by +1.9% in May from the same time last year, with condos down -0.7% as signals of a softer condo market grow louder

Condo prices are now down from last year in half of all major U.S. markets, with the largest declines along Florida’s Gulf Coast, plus Stockton CA, Austin, Memphis and Denver

There is much more in the mortgage monitor.