Lawler: Update on GSEs

From housing economist Tom Lawler:

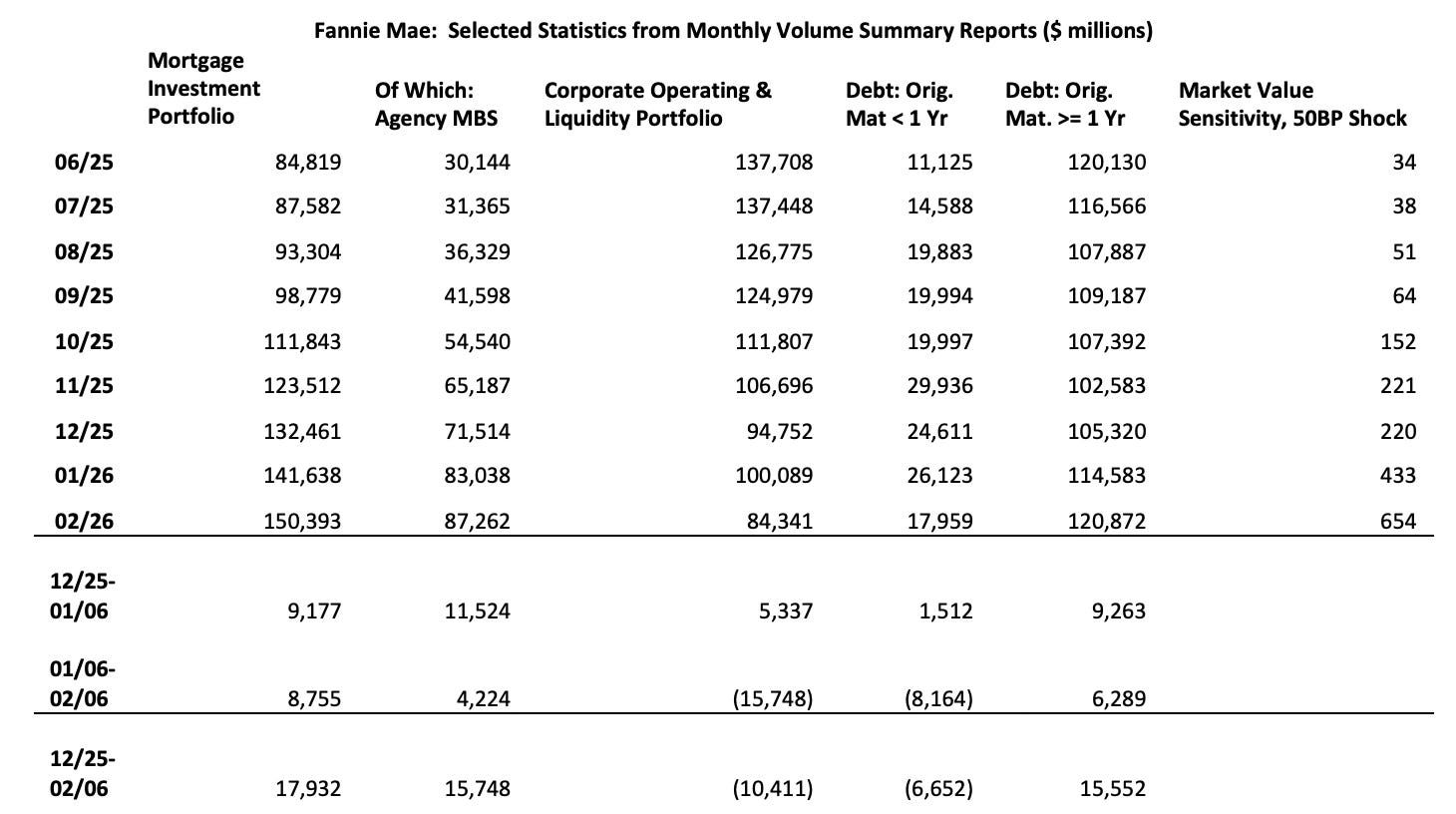

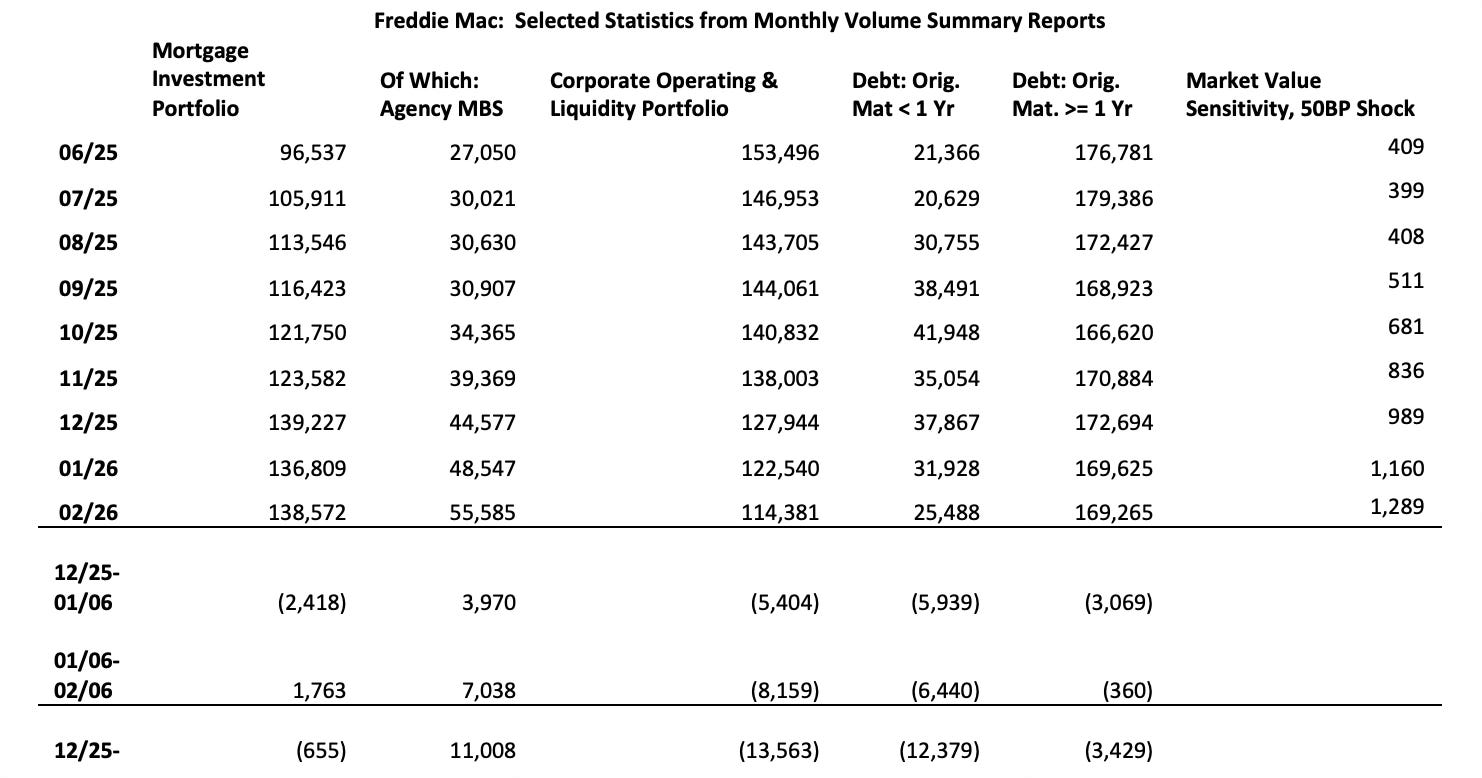

This week Fannie Mae and Freddie Mac released their monthly volume summary reports for February, and quite a few analysts were surprised about the quite modest increase in GSE agency MBS holdings last month, especially given the President’s post in January that the GSEs would buy $200 billion in MBS. Below are some summary stats from both GSE’s monthly volume summaries.

As these tables show, the two GSEs combined increased their Agency MBS portfolios last month by about $11.3 billion, less than the $15.5 billion increase in January and the smallest monthly increase since September 2025.

It should be noted that the GSE Agency MBS holdings in the monthly summaries reflected balances that have settled, while commitments to purchase MBS are typically for forward settlement. Having said that, however, if the GSEs had ramped up their commitments to purchase MBS soon after the President’s January 9th post, it’s hard to believe that February MBS balances would not have increased more than they actually did.

To be sure, there were ample reasons for the GSEs NOT to ramp up commitments to purchase MBS in January or February (or early March). After all, MBS/Treasury and MBS/Agency debt spreads were extremely low during this period (both nominal and option-adjusted), and debt-financed MBS purchases (or MBS purchases hedged with derivatives) during this period would have had extremely low (or negative) risk-adjusted returns on capital. However, some thought that political pressures from the hapless head of the FHFA would push the GSEs to make such purchases despite the fact that they would have been uneconomic.

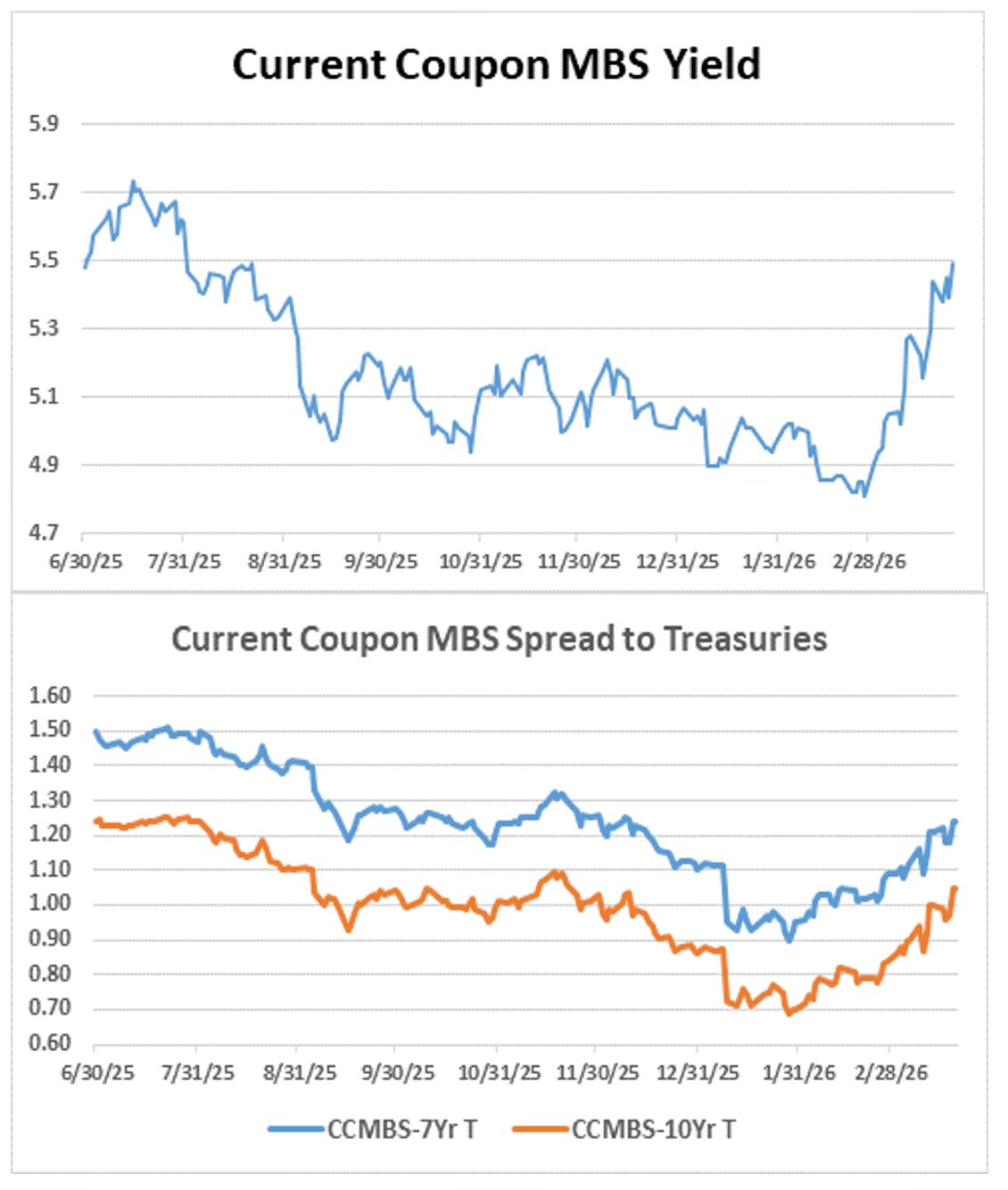

More recently, there was a press report from Bloomberg at the beginning this week that Fannie and Freddie had begun placing “sizable” orders to purchase MBS, though the report did not define “sizable” and the report was attributable to an unspecified “person with direct knowledge of the matter.” However, if true these “sizable” orders have not as yet resulted in lower MBS/Treasury spreads.

Moving back to the volume summaries, both Fannie and Freddie continued to reduce their corporate operating and liquidity portfolio last month, while debt outstanding at both companies declined on the month as well.

In re interest-rate risk, both companies market-value sensitivities to interest rate increases continued to rise last month, though the increases apparently reflect both companies’ decisions in the Spring/Summer of last year to increase the maturities/durations of their corporate operating and liquidity portfolios as opposed to “short-funding” mortgage holdings. Freddie Mac’s portfolio market value sensitivity to a 50 bp “shock” to interest rates increased sharply over the last years, from about $1 million in January 2025 to $1.289 billion at the end of February, with almost all of that increase reflecting an increase in the duration of its corporate operating and liquidity portfolio from less than one month in January 2025 to 36 months at the end of February. (Fannie Mae does not report the market value sensitivity of its corporate and operating liquidity portfolio sensitivity. In re these sensitivities, it’s worth noting that from the end of February to yesterday 3-year Treasury yields increased by about 60 bp.

This was from housing economist Tom Lawler.