Case-Shiller National Index up 19.1% Year-over-year in October

FHFA: "annual trends slowing over the last four consecutive months"

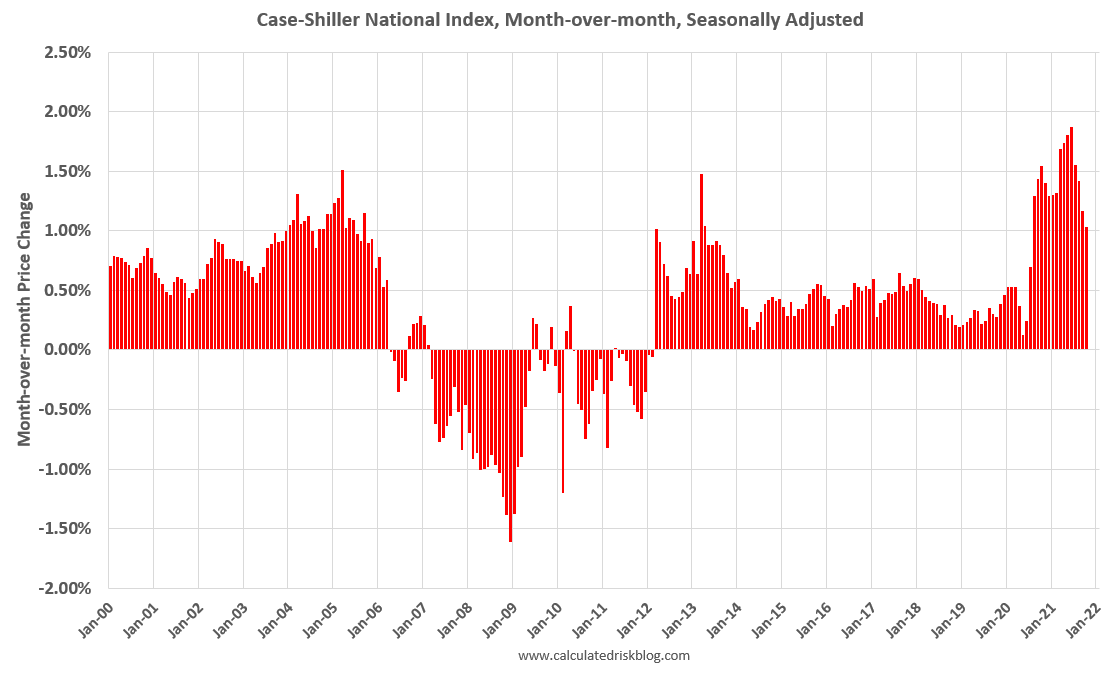

Both the Case-Shiller House Price Index (HPI) and the Federal Housing Finance Agency (FHFA) HPI for October were released today. Here is a graph of the month-over-month (MoM) change in the Case-Shiller National Index Seasonally Adjusted (SA).

The MoM increase in Case-Shiller was at 1.03%; still historically high, but lower than the previous 14 months. House prices started increasing sharply in the Case-Shiller index in August 2020, so the last 15 months have all been historically very strong, but the peak MoM growth is behind us - and the year-over-price growth is starting to decelerate.

FHFA House Price Index

On the FHFA index: FHFA House Price Index Up 1.1 Percent in October; Up 17.4 Percent from Last Year

House prices rose nationwide in October, up 1.1 percent from the previous month, according to the latest Federal Housing Finance Agency House Price Index (FHFA HPI®). House prices rose 17.4 percent from October 2020 to October 2021. The previously reported 0.9 percent price change for September 2021 remained unchanged. …

“House price levels continue to rise but the rapid pace is curtailing through October," said Will Doerner, Ph.D., Supervisory Economist in FHFA's Division of Research and Statistics. “The large market appreciations seen this spring peaked in July and have been cooling this fall with annual trends slowing over the last four consecutive months."

emphasis added

This is the monthly index. Here is a graph from the FHFA report showing the annual change by region for October 2021 compared to October 2020. Prices have increased sharply everywhere, but especially in the Mountain, Pacific and South Atlantic regions.

Case-Shiller House Prices

From S&P: S&P Corelogic Case-Shiller Index Reports 19.1% Annual Home Price Gain in October

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 19.1% annual gain in October, down from 19.7% in the previous month. The 10- City Composite annual increase came in at 17.1%, down from 17.9% in the previous month. The 20- City Composite posted an 18.4% year-over-year gain, down from 19.1% in the previous month. …

“In October 2021, U.S. home prices moved substantially higher, but at a decelerating rate,” says Craig J. Lazzara, Managing Director at S&P DJI. “The National Composite Index rose 19.1% from year-ago levels, and the 10- and 20-City Composites gained 17.1% and 18.4%, respectively. In all three cases, October’s gains were below September’s, and September’s gains were below August’s. That said, October’s 19.1% gain in the National Composite is the fourth-highest reading in the 34 years covered by our data. (The top three were the three months immediately preceding October.)”

emphasis added

This graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is up 0.8% in October (SA). The Composite 20 index is up 0.9% (SA) in October. The National index is 48% above the bubble peak (SA), and up 1.0% (SA) in October. The National index is up 100% from the post-bubble low set in February 2012 (SA).

The Composite 10 SA is up 17.1% year-over-year. The Composite 20 SA is up 18.4% year-over-year. The National index SA is up 19.1% year-over-year.

House Prices and Inventory

This graph below shows existing home months-of-supply (inverted, from the NAR) vs. the seasonally adjusted month-to-month price change in the Case-Shiller National Index (both since January 1999 through October 2021).

There is a clear relationship, and this is no surprise (but interesting to graph). If months-of-supply is high, prices decline. If months-of-supply is very low (like now), prices rise quickly.

In October, the months-of-supply was at 2.3 months, and the Case-Shiller National Index (SA) increased 1.03% month-over-month. The black arrow points to the October 2021 dot. In the November existing home sales report, the NAR reported months-of-supply decreased to 2.1 months in November.

We are seeing the expected deceleration in house price growth, and this trend will probably continue for at least a few more months (more on this tomorrow). My sense is the Case-Shiller National annual growth rate of 19.99% in August was probably the peak YoY growth rate, however, since the normal level of inventory is probably in the 4 to 6 months range - we’d have to see a significant increase in inventory to sharply slow price increases, and that is why I’m focused on inventory!

Please share with friends and colleagues, and please subscribe!