Lawler: Mortgage Rates Have Surged Since the Federal Reserve Cut Interest Rates Last Month

Lawler: Mortgage Rates Have Surged Since the Federal Reserve Cut Interest Rates Last Month

From housing economist Tom Lawler:

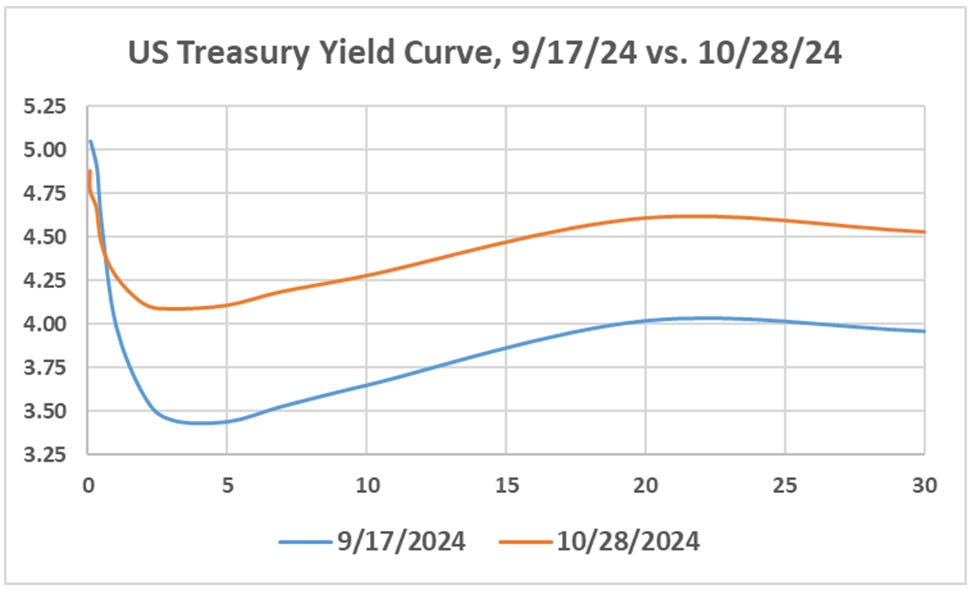

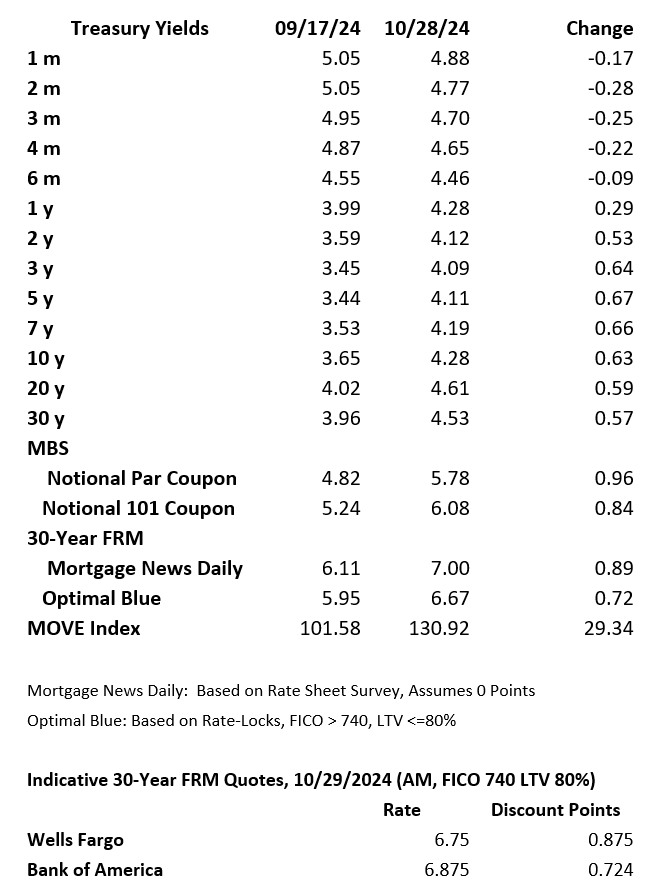

Folks who expected that mortgages rates would decline when the Federal Reserve began cutting its federal funds rate target range have been dazed and confused over the last month and a half. Since the day before the Fed’s 50 bp reduction in its funds rate target on September 18, 30-year MBS yields have surged by 84 to 96 bp, while mortgage rates have jumped by 72 to 89 bp. At the same time intermediate- and longer-term Treasury yields have risen 53 to 67 bp.

There are two main reasons MBS and mortgage rates have risen by more than Treasury rates over this period. First, implied interest rate volatility has surged, as many market participants were caught off-guard by the string of unexpectedly strong economic releases (and slightly higher inflation releases) following the Fed’s rate decision. For example, the BofAML MOVE index, a measure if implied interest rate volatility derived from one-month options on Treasuries across the yield curve, increased from 101.58 on September 17 to 130.92 on October 28, its highest reading since October 30, 2023. (Mortgage investors effectively write a prepayment option to home borrowers, and as such higher implied interest rate volatility increases the premium over Treasuries that investors require to compensate them for prepayment risk.)

And second, MBS option-adjusted spreads, which were at the low-end of the “no Fed MBS intervention” range just prior to the Fed’s action, have since moved higher.

Below are Treasury yields, MBS yields, Mortgage Rates, and the MOVE Index for 9/17/2024 and 10/28/2024, as wells as indicative 30-year fixed-rate mortgage quotes from Wells Fargo and Bank of America for the morning of October 29, 2024.

CR NOTE: The above was from housing economist Tom Lawler. As Lawler noted last week, estimates of the “Neutral” rate have been increasing. Lawler wrote:

Based on an assessment of various measures, my best is that the neutral real interest rate in the US is between 1 ¾% to 2%. One of course needs to add inflation/inflation expectations to that range. If/when the Fed were to achieve its 2% inflation target, then the neutral nominal interest rate would be 3 ¾% to 4%.

Factor in a normal yield curve (longer rates higher than short rates), and a more normal spread from the 10-year yield to 30-year mortgage rates, and you can see why there is a new normal range for 30-year mortgages.

See from June 2023: Could 6% to 7% 30-Year Mortgage Rates be the "New Normal"? and an update in August 2023: The "New Normal" Mortgage Rate Range