NMHC on Apartments: "Looser market conditions for the ninth consecutive quarter"

NMHC on Apartments: "Looser market conditions for the ninth consecutive quarter"

Leading indicator for Rents and Apartment Vacancies suggests more weakness for Apartments

Apartment market conditions showed signs of improvement in the National Multifamily Housing Council’s (NMHC’s) October 2024 Quarterly Survey of Apartment Market Conditions. All but the Market Tightness (37) index indicated more favorable conditions this quarter, with Sales Volume (67), Equity Financing (63) and Debt Financing (77) all coming in above the breakeven level (50).

“The 10-Year Treasured yield fell 28 basis points (bps) over the past three months as the Federal Reserve enacted its first, 50 bps cut to short-term rates,” noted NMHC’s Economist and Senior Director of Research, Chris Bruen. “Survey respondents, in turn, reported more favorable conditions for debt financing for the third straight quarter and more available equity financing for the first time in two and a half years.”

“Elevated levels of multifamily deliveries, however, resulted in the ninth consecutive quarter of looser conditions, especially in the South and in Sun Belt markets. Still, strong demand for apartments has meant that much of this new supply is getting absorbed.”

The Market Tightness Index came in at 37 this quarter – below the breakeven level of 50 – indicating looser market conditions for the ninth consecutive quarter. While close to half of respondents (46%) thought market conditions were unchanged relative to three months ago, 40% of respondents thought markets have become looser, up from 27% in July. Fifteen percent of respondents reported tighter markets than three months ago.

The Sales Volume Index reading of 67 reflected a third straight quarter of increasing deal flow. As was the case last quarter, the plurality of respondents (46%) reported sales volume to be unchanged from three months ago. Forty-three percent of respondents reported higher sales volume this quarter, increasing from 21% of respondents in April and 32% in July, while 10% thought volume was lower.

The Equity Financing Index flipped this quarter with a reading of 63 – the first quarter of more available equity financing since January 2022. Thirty-two percent of respondents this round reported more available equity financing, up from 13% in July, while just 6% thought it less available. Roughly half of respondents (53%) thought availability remained unchanged from three months ago.

The Debt Financing Index also came in above the breakeven level of 50 – indicating more favorable conditions for debt financing compared to three months ago – with a reading of 77. Up from 37% in July, the majority of respondents this quarter (62%) felt now was a better time to borrow than three months ago, while 8% thought borrowing conditions were worse than three months ago. A quarter of respondents reported unchanged debt financing conditions, down from 44% last quarter.

Emphasis added

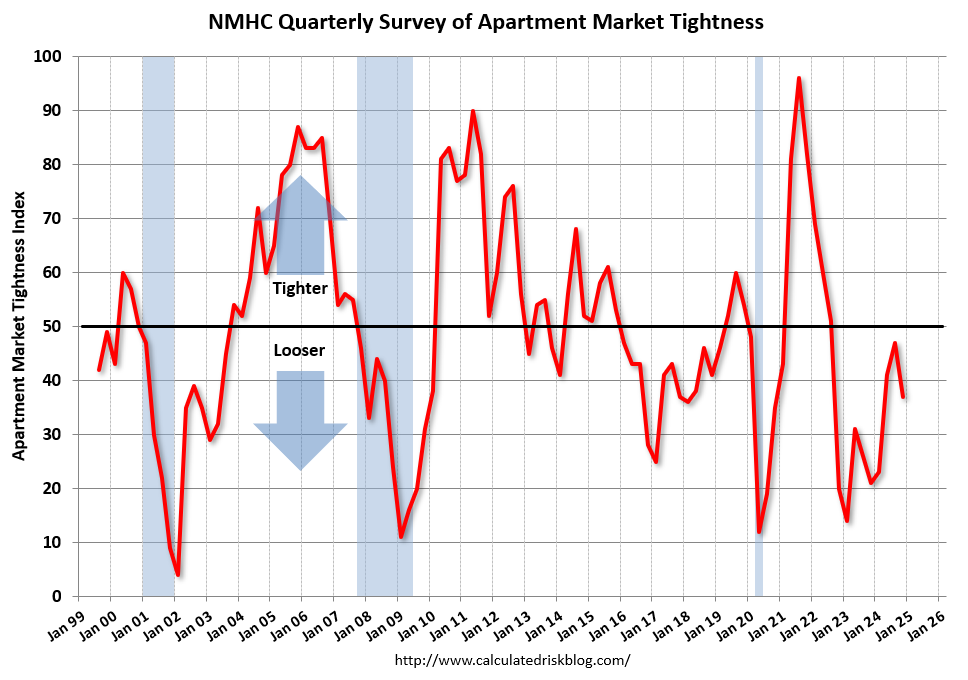

This graph shows the quarterly Apartment Tightness Index.

The quarterly index decreased to 37 in October from 47 in July. Any reading below 50 indicates looser conditions from the previous quarter.

This index has been an excellent leading indicator for rents and vacancy rates, and this suggests higher vacancy rates and a further weakness in asking rents. This is the ninth consecutive quarter with looser conditions than the previous quarter.

The NMHC tightness survey, combined with the Architectural Billings Index that has shown a decline in multi-family design billing for twenty-five consecutive months, suggests multifamily starts will remain under pressure.

As I noted last week in Housing Starts Decreased to 1.354 million Annual Rate in September, this quarterly survey from the NMHC and the monthly Architectural Billings Index (to be released this week) are excellent leading indicators for the multi-family sector and should be watched for any signs of a future pickup in multi-family starts.